An empirical study of the effect of venture capital participation on the accounting information quality of IPO firms

2012-06-27 05:48ZhiyingHuWeixingCaiJinjinHanRulaSa

Zhiying Hu,Weixing Cai,Jinjin Han,Rula Sa

DongLing School of Economics and Management,University of Science and Technology,China

An empirical study of the effect of venture capital participation on the accounting information quality of IPO firms

Zhiying Hu*,Weixing Cai,Jinjin Han,Rula Sa

DongLing School of Economics and Management,University of Science and Technology,China

A R T I C L EI N F O

Article history:

Accepted 29 August 2012

Available online 6 October 2012

JEL classification:

G32

Venture capital

Earnings management

IPO

Lock-up period

Using a sample of IPO companies on the Shenzhen Small and Median Enterprise Board and the ChiNext Stock Market between 2005 and 2009,this paper analyzes the effect of venture capital participation on accounting information quality.We find that venture capitalists have a significant effect on earnings management,with reduced discretionary accruals before the expiration of the equity lock-up period and enhanced discretionary accruals after the expiration of the equity lock-up period.Our findings support the moral hazard hypothesis of venture capital,but not the certification/monitoring role of venture capital in IPOs.In addition,we find that venture capital plays a more important role in the earnings management of non-state-owned IPO companies than of state-owned companies.

Ⓒ2012 China Journal of Accounting Research.Founded by Sun Yat-sen University and City University of Hong Kong.Production and hosting by Elsevier B.V.All rights reserved.

1.Introduction

China’s venture capital market has recently witnessed tremendous development under the influence of capital internationalization and with support from the government.Venture capital(VC)generally refers to medium-and long-term capital that is invested in unlisted enterprises and that gains investment returns throughIPOs,mergers,acquisitions,liquidations and transferring the equity of portfolio firms.1In fact,VC refers to investment in the early stages of an enterprise.However,due to the short history of the venture capital market, many VCs not only perform early-stage investment,but also pre-IPO investment.As it is hard to discriminate between them,we include both types of VC in this study.IPOs are the most popular exit strategy because they bring the highest returns on VC investments.Thus,venture capitalists (VCs)are the main participants in IPO activities and their behavior has a significant influence on the operation of the capital market.Accounting information is one of the major sources of information for the capital market.Higher accounting information quality makes the allocation of capital market resources more efficient and gives investors more protection.Therefore,to protect investors more effectively,the effect of the participation of VCs on the accounting information quality of IPO firms has received much attention.

Based on the framework of asymmetric information,Barry et al.(1990)and Sahlman(1990)proposed the certification/monitoring hypothesis.Under this hypothesis,VCs as professional investors play a certification role in the identification of the portfolio firm’s intrinsic value.To reduce agency costs and increase the value of portfolio firms,VCs as large shareholders will actively monitor the portfolio firms,including their accounting information quality.Compared to companies without VC support,the earnings quality of VC-backed IPO companies should be better.In contrast,Gompers(1996)and Lee and Wahal(2004)argue that the limited lifetime and special organizational structure of IPO companies mean that VCs must pay attention to how to get back their original investment and receive high returns,so VCs are likely to participate in portfolio firms’IPO activities opportunistically and have moral hazard problems.This hypothesis implies that VCs may collude with2According to Chemmanur and Loutskina(2007),VCs often maintain close relationships with underwriters.portfolio firms or exert pressure on management,using their own professional advantages or social networkswith underwriters and government,to help the management of IPO firms manage accounting earnings before and during the IPO,thereby increasing the IPO price and increasing their investment return following the IPO.

Institutional theory holds that the beliefs,goals and behavior of individuals and groups are influenced by various institutional environments(Scott,1987,1995).Particular institutional environments will inevitably lead to particular venture capital IPO behavior,including the effect on accounting information quality in IPO companies.Compared with the US market,China’s market has some special features.For example, the Chinese government provides considerable guidance and support for VCs to promote innovation.In September 1985,the State Council officially approved the establishment of the New Technology Venture Investment Company,China’s first franchised venture capital company.Since then,many VCs have been established with the support of local governments,such as Beijing Venture Capital,Shanghai Venture Capital, Suzhou High-tech Investment Company and the Shenzhen High-tech Investment Company(Chen et al., 2011).However,the development of VCs in the US market is guided by market forces.Meanwhile,China’s stock market is a newly emerging market with a short history and relatively weak investor protection.Thus,to encourage long-term shareholding by VCs and reduce the negative effects of equity selling immediately after an IPO,the China Security Regulation Committee(CSRC)mandated a lock-up period regulation,which states that VCs are not allowed to sell their equity until at least 12 months after the IPO.In contrast,VCs in the US market can sell their equity immediately after the IPO.

Most extant studies in this area are based on the mature Anglo-American market environment.Although some research focuses on emerging Asian markets,few studies discuss China’s market specifically.In this study,we use medium and small IPO firms in China from 2005 to 2009 as our sample,to study the participation of VCs on VC portfolio firms’earnings management 1 year pre-IPO,in the IPO year and 1 year post-IPO,thus allowing a comprehensive analysis of the effect of VCs on accounting information quality before and after the expiration of the lock-up period.After controlling for the sample self-selection endogeneity problem,we find that the participation of VCs affects the earnings management of IPO firms.Earnings management is lower before the expiration of the lock-up period and higher after the lock-up period expires. The empirical evidence thus supports the moral hazard hypothesis.Furthermore,due to financing bottlenecks and the poor corporate governance of non-state-owned enterprises,the participation of VCs has a greater effect on the extent of earnings management for non-state-owned enterprises before and after the expiration of the lock-up period.

The remainder of this paper proceeds as follows.Section 2 reviews the related literature,analyzes the institutional background in China and develops the hypotheses.Section 3 describes the research design and introduces the data and variables.Section 4 presents the empirical results.Section 5 concludes the paper.

2.Literature review and research hypotheses

There are two hypotheses on the effect of VCs’participation in their portfolio companies’IPOs:certification/monitoring hypothesis and moral hazard hypothesis.These two hypotheses have different implications for the effects of VC participation on the accounting information quality of IPO companies.Most studies use earnings management as a proxy for accounting information quality,which refers to the behavior of increasing accounting earnings in the current period by means of accounting accruals and real transaction arrangements.Lower earnings management means higher accounting information quality.

In the US market,VCs are allowed to sell the shares of portfolio companies immediately after their IPO and an IPO is the first opportunity for a private firm to raise equity from dispersed investors.Therefore,most of the studies based on the US market focus on the effect of VC participation on accounting information quality in the pre-IPO and IPO process.The certification/monitoring hypothesis predicts that to reduce agency costs and establish their professional investor reputation,VCs should be actively involved in corporate governance,including monitoring and motivating portfolio firms’managers,which at the same time reduces the conflict of interest between inside and outside investors(Baker and Gompers,2003).This also means that VCs should monitor accounting information quality,which is an important part of corporate governance.There is some evidence to support this view.For example,Ball and Shivakumar(2005)find that information disclosure in the IPO process is highly regulated.Although earnings management and less conservative information disclosure increase pre-IPO,this is reversed after the IPO,bringing serious economic consequences if discovered by the market.Thus,to meet stock market requirements,private companies in the United Kingdom tend to report more conservative accounting information several years prior to their IPO.The companies backed by VC are influenced more by this force,because VC backing increases the predictability of listing compared with non-VC-backed firms.Therefore,in the process of going public,VC-backed firms disclose losses as early as possible to satisfy the future requirement of timely disclosure of information,which results in more conservative accounting information and less earnings management.Gioielli et al.(2008)compare the pre-IPO and IPO discretionary accruals of VC-backed firms with those of non-VC-backed firms and find that the earnings management of VC-backed firms is less than that of non-VC-backed firms.Hochberg(2003),Morsfield and Tan(2006)and Katz(2009)report similar findings.Moreover,VC-backed firms also have lower discretionary accruals after IPO(Gioielli et al.,2008)and a lower likelihood of financial restatements(Agrawal and Cooper, 2009).Accounting information quality also increases with the participation of more reputable and older VCs (Agrawal and Cooper,2009).

However,as an IPO is the first time a private firm can raise equity from public investors,it also magnifies the VC’s investment value,which exacerbates the moral hazard problem.To ensure a higher IPO price and obtain higher returns on the sale of their equity during and after IPOs,VCs will help portfolio firms to manage earnings,which leads to lower accounting information quality and further increases conflicts between insider stakeholders and outsider investors.This view is also supported by a number of studies.For example, Darrough and Rangan(2005)find that VC-backed firms reduce R&D expenditures during the IPO year to ensure higher accounting earnings.In addition to R&D expenditure arrangements,discretionary accruals have also been used as a measure of earnings management.Using reverse leveraged buyouts as their sample,Chou et al.(2006)find sample firms manage earnings by discretionary accruals in the IPO year.Furthermore, Wongsunwai(2007)documents that only the highest-quality VCs inhibit earnings management by means of discretionary accruals,real transaction arrangements and financial restatements in IPOs.At the same time, as VCs usually occupy seats on their portfolio firms’boards,are involved in their management and get the information they need directly,they lack the incentive to monitor the quality of accounting information. Hence,earnings management is not necessarily lower in VC-backed IPO companies and as the value of the VC’s stakeholding increases,the information content of accounting earnings declines further(Cohen and Langberg,2006).

The institutional environment has an influence on the behavior of economic entities.China’s institutional environment has some special features as follows.First,under the influence of China’s traditional culture,VCs give more help to portfolio firms in the establishment of social relations than in the provision of value-added services.Hu and Bu(2012)show that companies backed by VCs with political connections are more likely to have successful IPOs than companies backed by VCs with no political connections and only a few VCs help portfolio firms to form strategic alliances with VCs’parent companies or other companies.These factors increase VCs’moral hazard in earnings management during IPO.Second,as mentioned above,most VC companies in China are owned by the government.Government-backed VCs are thus influenced by their public functions,which reduces the incentive for VCs to monitor their portfolio firms as active shareholders.At the same time,VC companies in China are often organized as limited liability corporations,which incur more agency costs than partnerships,thus further reducing monitoring efficiency.Additionally,China’s capital market is an emerging market without a long history.Although the regulatory systems are being improved,there are still some problems with the market mechanism and support systems,which result in low investor protection and further exacerbate the moral hazard problem of VCs.

As the supply of venture capital cannot satisfy the current market demand in China,the reputation effect cannot reduce the moral hazard of VCs in the current environment.At the same time,the rapid changes in the regulatory systems of emerging capital markets mean reduced safety for market participants.Therefore,to realize their investment returns as early as possible,VCs will shorten the equity duration before the IPO and sell their equity as soon as possible after the expiration of the lock-up period.If the pre-IPO duration is not long enough,it is hard for VCs to establish a relationship with the portfolio firm and to be involved in its operations and management during the IPO(Cao,2009).However,our results show that in about 41%of portfolio firms,the lead VCs hold equity for less than 2 years pre-IPO and in about 10%of cases for less than 1 year.For example,Huijin Lifang and Jinshi Investment were the two venture capital firms that supported Shenzhou Taiyue.The duration of both companies’pre-IPO equity holding was 165 days.Furthermore,selling equity immediately after the IPO can be a convincing interpretation of the opportunism of VC participation in the IPO.We find that almost 21%of VC-backed firms incur equity selling immediately after the expiration of the lock-up period.For example,Tongzhou Electronics held its IPO on June 27,2006,but incurred equity selling by Dachen Venture,its VC investor,on June 27,2007-the exact date that the lock-up period expired.The same thing happened with Western Material:on the first day after the expiration of the lock-up period,its VC,Shenzhen Innovation Investment,cashed in some of its equity.

The governance role played by the media in China’s capital market has been well documented(Li and Shen, 2010;Yu et al.,2010).The publicity given to the success stories of VC-backed entrepreneurs encourages more entrepreneurs to seek help from venture capitalists.Entrepreneurs will favor VCs with better reputations. Accordingly,VCs have an incentive to provide value-added services to portfolio firms to establish their professional reputation.Furthermore,some foreign-owned VCs use their previous investment experience to monitor the portfolio firms before and after the IPO,so that they can play a certification/monitoring role.

The above two forces will have opposite effects on the participation of VCs in an IPO,and will also have different effects on the accounting information quality of IPO companies.As the above analysis shows,the lock-up period in China’s market means that VCs sell their equity after the expiration of the lock-up period, thus the key processes in the effect of VC participation on accounting information quality include the IPO and the expiration of the lock-up period.The pattern of portfolio firms’IPO earnings management changes accordingly.

If certification/monitoring is dominant,VCs will not only inhibit earnings management before and during the IPO to enhance accounting information quality and reduce the conflict between inside and outside investors,but they will also certify and monitor the portfolio IPO firms and inhibit the earnings management induced by the insider trading of management and other non-controlling stakeholders after the expiration of the lock-up period.However,if moral hazard is dominant,VCs will inevitably pay less attention to the IPO process,because the relevance of the relationship between the IPO price and the VC’s investment return decreases during the lock-up period,and focus more on equity selling after the expiration of the lock-up period.Due to the interaction between accounting earnings in consecutive periods,VCs will treat the IPO and the expiration of the lock-up period as a whole and design a dynamic earnings management strategy.In order to reverse accounting earnings in the year in which the lock-up period expires,the earnings management ofVC-backed companies before the expiration of the lock-up period will not be higher than that of non-VC-backed firms.Because VCs in China’s market tend to select firms with high growth and excellent financial performance(Bruton and Ahlstrom,2003),the appropriate reduction in accounting earnings before and during the IPO will not have a significant effect on IPO pricing.Meanwhile,improvements in the IPO regulatory system have increased the cost of earnings management(Xu and Chen,2009).Thus,the earnings management of VC-backed firms before the lock-up period expires will be even lower than that of non-VC-backed firms. Based on the above analysis,we propose our first hypotheses.

Hypothesis 1.The participation of VCs will influence earnings management before and after the expiration of the lock-up period.

Hypothesis 1a.The participation of VCs will reduce earnings management before the expiration of the lockup period(i.e.,1 year before the IPO and the IPO year itself)and the year in which the lock-up period expires (i.e.,1 year after the IPO).

Hypothesis 1b.The participation of VCs will increase earnings management in the year of the lock-up period expiration(i.e.,1 year after the IPO)and reduce earnings management before the expiration of the lock-up period(i.e.,1 year before the IPO and the year of the IPO itself).

In China,state-owned enterprises have a natural relationship with banks,which gives them advantages in accessing bank loans.In a survey of rural commercial banks in Jiangsu and Zhejiang provinces,Brandt and Li (2003)show that banks treat enterprises with different types of ownership differently when awarding bank loans,indicating“financial discrimination.”Fang(2010)compares state-owned industrial enterprises and foreign-funded industrial enterprises,and further documents the existence of“financial discrimination”in the process of allocating bank loans.The result of financial discrimination is that non-state-owned enterprises in need of funding find it more difficult to obtain bank loans,thus increasing the demand for funds.Under this circumstance,VCs that can provide development funds to non-state-owned enterprises will have stronger bargaining power in their negotiations with them.Meanwhile,Chemmanur and Loutskina(2007)find that VCs help to market their portfolio firms to analysts,investment banks and institutional investors.We believe that non-state-owned enterprises with fewer political connections have a stronger need for the marketing power of VCs during the IPO process,thus further increasing the bargaining power of VCs.Therefore, VCs will have a more significant influence on the corporate governance,operations and financial behavior of non-state-owned enterprises than on state-owned enterprises.

According to Hao et al.(2011),during the 30 years since China’s reform and opening-up,state-owned enterprises have experienced the decentralization reform,contracting reform,joint-stock pilot,and modern enterprise system reform.They have developed into new state-owned enterprises with“clear property rights, well-defined power and responsibility,separation of political function and business operation,scientific management.”The governance structure of state-owned enterprises has further improved,especially since the establishment of the State-owned Assets Supervision and Administration Commission in 2003.Using enterprises in Shandong Province from 2002 to 2009 as their sample,they show that the total governance efficiency3In their paper,total enterprise governance efficiency is measured as the sum of operational efficiency aimed at making profits and functional efficiency for the purpose of maximizing social welfare.of state-owned enterprises,with the exception of enterprises wholly owned by the state,is better than that of non-state-owned enterprises and foreign enterprises.Gao and Cai(2011)also find the financial governance of state-owned listed companies to be significantly better than that of non-state-owned listed companies.Therefore,we argue that the more robust system in new state-owned enterprises inhibits the negative effect of VC participation on enterprises under the new regulatory environment.This leads to our second hypothesis.

Hypothesis 2.VC participation has a greater effect on earnings management before and after the lock-up period for non-state-owned enterprises than for state-owned enterprises.

3.Research design

3.1.Sample selection

As the lock-up period for most VCs is 1 year according to the CSRC,we select 1 year after IPO as the year of the expiration of the lock-up period(referred to as the post-IPO year).Because accruals in the year before IPO and the IPO year provide a valid test of earnings management(Teoh et al.,1998;Ball and Shivakumar, 2008),we use discretionary accruals in these 2 years as our measure of accounting information quality before the expiration of the lock-up period.We use a sample of 323 companies that held their IPO on the Shenzhen Small and Medium Enterprises Board(SME Board)and the Growth Enterprise Market(GEM)between 2005 and 2009.We delete IPO firms with the two-digit SIC code C2 because there are fewer than 10,making it hard to get an appropriate estimation of discretionary accruals.We also delete one other company with missing financial data.Finally,we have a sample size of 320 companies in each firm year.We obtain detailed VC data by checking the information from the CV-source with the prospectus,obtain financial data from the Wind database,prospectus and annual reports,and the rankings of underwriters and auditors from the websiteof the industry committee.Panel A of Table 1 reports the sample selection process,Panel B shows the VC-backing frequency and Panel C shows the industry distribution.

Table 1Sample selection.

Panel A of Table 1 shows that the stock market boom in 2007 led to 101 IPOs in that year,which was the highest number during the five consecutive sample years.The second highest was 90 IPOs in 2009,the year that China launched GEM.Panel B reports the descriptive results for the number of sample firms that received VC-backing.It seems that VCs participated actively in the capital market,with one third of IPOs backed by VCs.The percentage of firms backed by VCs increased throughout the period,reaching 55.56%in 2009. According to Panel C,VCs give more support to the electronics industry,the machinery,equipment and instrument industry,and the information technology industry.The percentages of VC-backed sample firms in these three industries are 16%,28.57%and 17.86%respectively,and the proportions in the overall sample are 9.69%,20.94%and 11.56%.

3.2.Research design

According to Katz(2009),we use the following model to test the effect of VC participation on the earnings management of IPO firms:

In Model(1),the dependent variable DAtrepresents the discretionary accruals of IPO firms in year t.We use a cross-sectional modified Jones model to calculate DAt.To obtain DAt,we first use the listed companies in the same industry as each IPO sample firm to estimate the parameters in the following equation:

where ACCt=NIt-CFOt,ACCtis total accruals in year t,NItis total income in year t,CFOtis net cash flow from operations;At-1is total assets in year t-1;ΔREVtis change in sales between year t and year t-1; ΔRECtrepresents the change in account receivables from t-1 to t;PPEtis total fixed assets in year t;and εtis the residual.We then insert the estimated coefficients^β1,^β2and^β3into the following equation,to obtain the non-discretionary accruals(NDAt)of sample firms in year t:

Next,we calculate the total accruals of sample firms in year t:ACCt=NIt-CFOt. Finally,we obtain the discretionary accruals(DAt)of sample firms in year t using the following equation:

The dummy variable VC is the key variable.If a sample firm is supported by VC,VC equals 1,otherwise 0. In this model,if the pre-IPO year and the IPO year regression results show that the coefficient a1is signif icantly negative or not significant and the coefficient a1in the post-IPO year is significantly positive,then VCs’moral hazard is dominant.On the contrary,if the a1coefficients in the three regressions are all signif icantly negative,the VCs’certification/monitoring role is dominant.

Because financial performance is a key factor in IPO decisions and whether a company can get support from a VC is determined by its financial performance,performance-matched discretionary accruals can control for the systematic difference between the performance of VC-backed and non-VC-backed IPO firms. Thus,performance-matched discretionary accruals are more relevant in this study.We also calculate performance-matched discretionary accruals(Kothari et al.,2005)to measure earnings management,in accordance with Morsfield and Tan(2006).Performance-matched discretionary accruals are calculated as follows:first,we obtain the ROA of each listed company for each year4For each sample firm in industries with the SIC code C,we select an ROA-matched firm from the sample firms with the same two-digit SIC.from 2005 to 2009;and second,we match each sample firm with a non-IPO firm with the same one-digit SICcode and that has the closest ROA to the sample firm.We then calculate the performance-matched discretionary accruals as the difference between the discretionary accruals of each IPO firm and the discretionary accruals of the matched firm.

In addition,we control for a number of factors that may affect earnings management,including the size of the IPO company,growth,financial leverage,quick ratio,cash flow performance,ownership and the reputations of the IPO auditors and the underwriter.Our reasoning is as follows.First,because firms with high growth may lack cash,accruals and discretionary accruals in these firms may be larger.Second,firms with higher financial leverage receive more monitoring from debtors,so their earnings management will be lower. Third,the quick ratio represents short-term financial flexibility;firms with more financial flexibility may have more cash and lower accruals,and this will further influence their discretionary accruals.Fourth,given that net income is constant,the adequacy of cash flow directly affects the level of accruals,thus affecting the level of discretionary accruals.Fifth,accounting information quality will be better if the company is audited by more reputable auditors,and the underwriter’s reputation may influence the choice of auditor.Seventh,different ownership may also affect earnings management,as documented in previous studies.Finally,firm size can proxy for a firm’s resources to influence accounting earnings.

We recognize that Model(1)does not control for the endogeneity problem arising from sample self-selection,because a VC’s choice to invest in a certain firm may not be random.The control variables in Model(1) cannot reflect this tendency.Therefore,even when earnings management has no relationship with VC participation,the regression result may still show that VC participation has a significant effect on earnings management,and vice versa.

For example,we assume the following equation:

where Y represents earnings management,C is a dummy variable that equals 1 for listed companies that receive VC support and 0 otherwise,and X is a proxy for all other factors that may influence earnings management.Because the decision of a VC is based on a number of factors,we use a related model to reflect this decision:

where C*is an unobserved latent variable.The decision we observe is C=1,if C*>0,otherwise C=0.

If this sample self-selection problem exists,the coefficient δ we estimate by OLS will not measure the effect of the participation of VCs appropriately.In empirical studies,this self-selection problem can be solved by using a treatment effect model(Greene,2003).

We use a self-selection model to control for this potential endogeneity problem.Specifically,the participation of VCs may be affected by sales per share,net assets per share,total assets per share and other financial factors of portfolio firms(Morsfied and Tan,2005).It may also be influenced by industry factors,as VCs tend to invest in firms in high-tech industries(Lee and Wahal,2004).Therefore,we use a dummy variable to capture whether the sample firms are in a high-tech industry.Finally,according to Lerner(1995),VCs tend to invest in firms close to their geographical location to reduce their costs.Because VCs in China are concentrated in Beijing,Guangdong,Jiangsu and Zhejiang,a dummy variable is used to proxy for whether the sample firms are registered in such provinces.We regress VC on the above five variables to estimate the self-selection model.

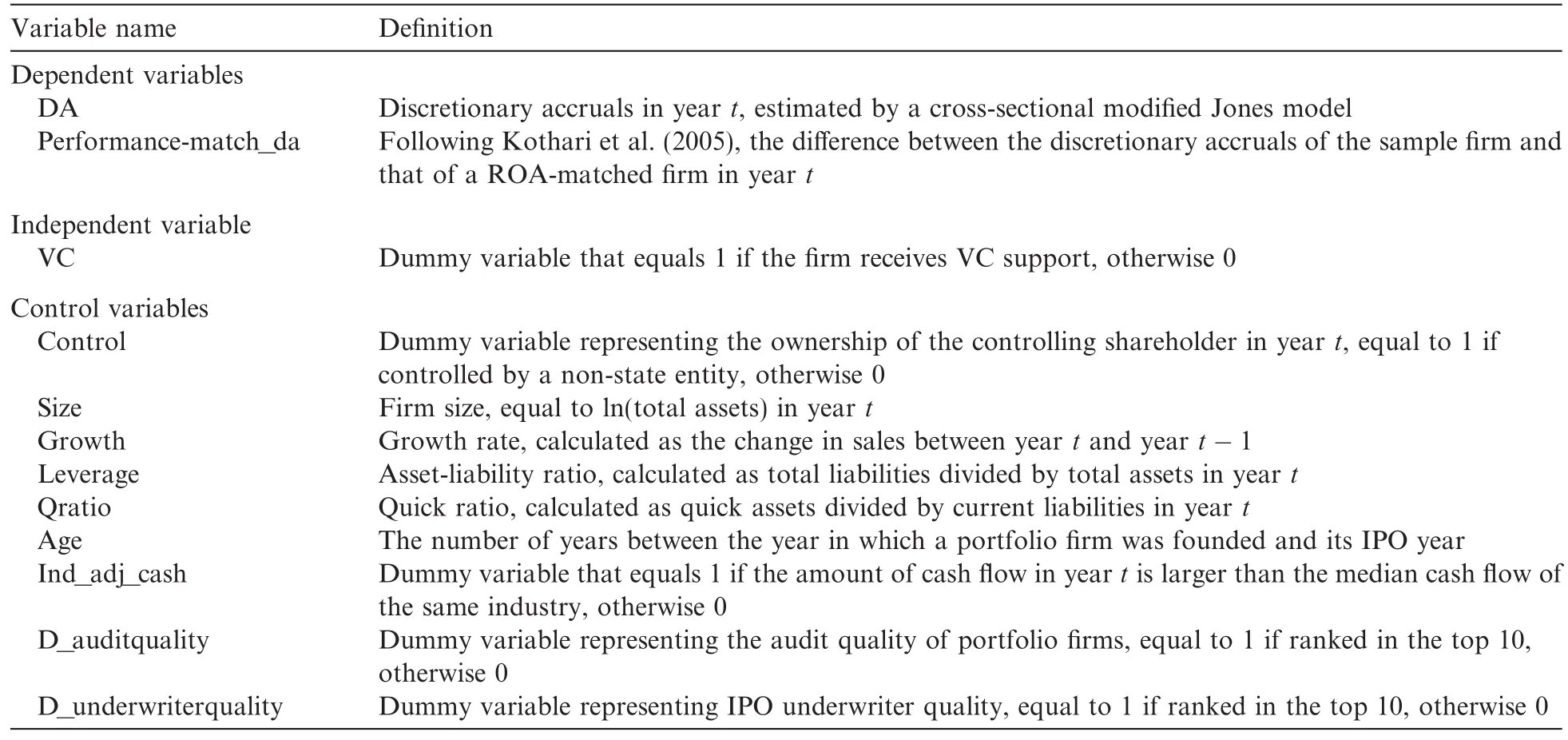

Table 2 shows the definitions of the variables used in this paper.

4.Empirical results

4.1.The participation of VCs in earnings management of IPO firms

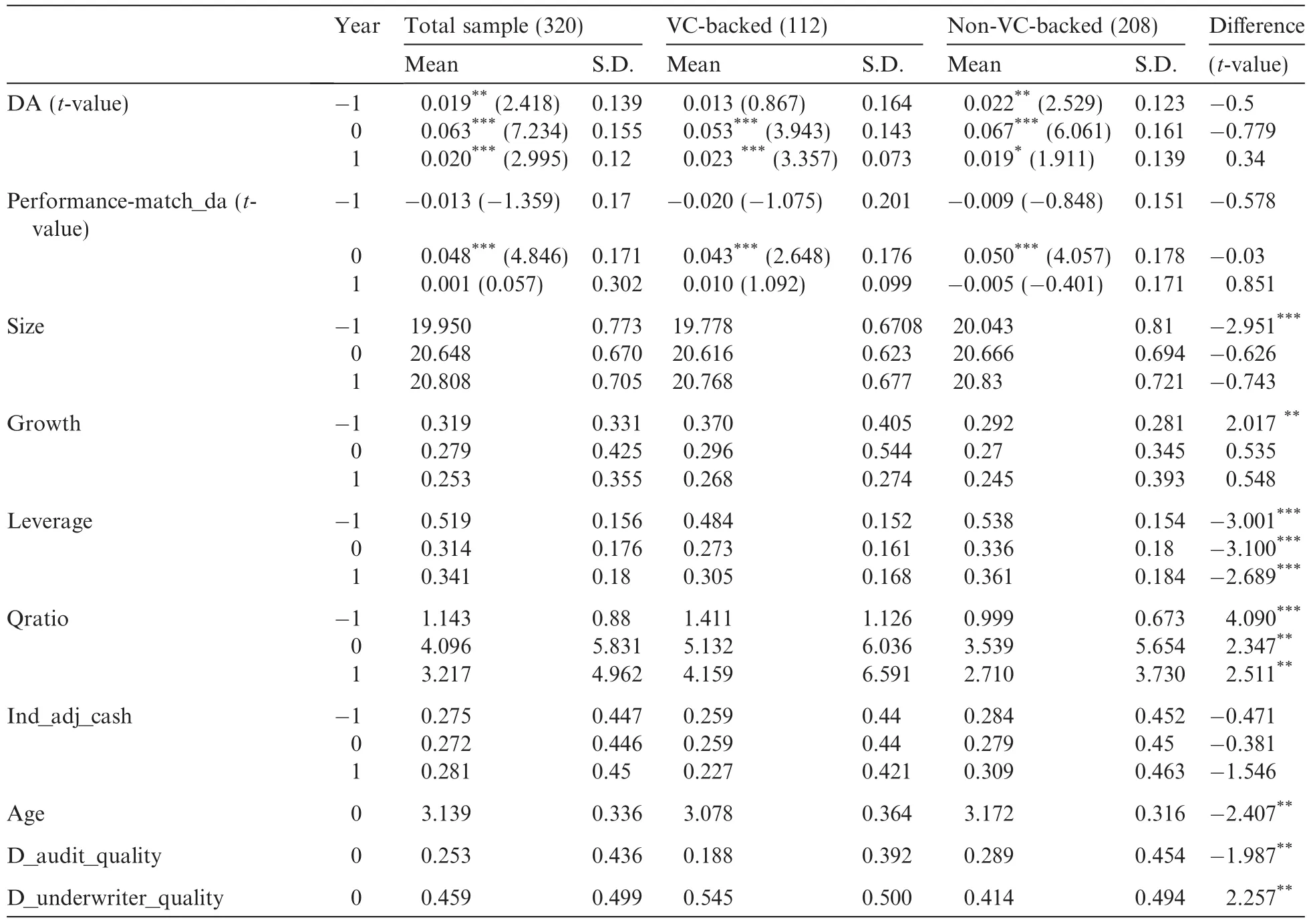

Table 3 shows the descriptive statistics for the independent and control variables.In summary,both discretionary accruals estimated by a cross-sectional modified Jones model and performance-matched discretionary accruals in the pre-IPO,IPO and post-IPO years tend to increase at first and then decline.They peak in the IPO year and are higher in the post-IPO year than in the year before the IPO.Discretionary accruals estimated by a cross-sectional modified Jones model are positive in all three consecutive years,significant at the 5%,1%and 1%levels,respectively.However,only performance-matched discretionary accruals in the IPO year are positive at the 1%signi ficance level.Performance-matched discretionary accruals are negative in the pre-IPO year and positive in the post-IPO year.In summary,we conclude that sample firms manage earnings during the IPO process,especially in the year of the IPO and the year in which the lock-up period expires.

Except for controlling shareholders,the lock-up period for other insiders,including management,is 1 year in China.For firms listed in the first half of the year,accounting earnings at the end of the IPO year will directly in fluence the selling price,so they have an incentive to increase accounting earnings in the IPO year. However,for those listed in the second half of the year,accounting earnings in the year following the IPO will have more of an effect.Therefore,to analyze the incentives of earnings management in the IPO year and the following year,we further divide our sample into two subsamples according to whether they were listed in the first or second half of the year.We also de fine a firm as having high earnings management if its discretionary accruals are above the sample median.We then investigate the relationship between earnings management and the time of listing.We find that in the IPO year,for firms listed in the first half of the year,the proportion of high earnings management firms-measured by discretionary accruals estimated by a cross-sectional modi fied Jones model(performance-matched discretionary accruals)-is 61.9%(5Due to space limitations,we do not report this result.8.65%).For firms listed in the second half of the year,the proportion is 43.98%(45.83%)and the difference is significant at the 1%(5%)level.In the year of the lock-up period expiration,the proportion of firms de fined as having high earnings managementmeasured by discretionary accruals estimated by the cross-sectional modi fied Jones model-is 43.26%.For firms listed in the second half of the year,the proportion is 53.24%and the difference is significant at the 10%level.The results for performance-matched discretionary accruals show the same pattern:the proportion of firms listed in the first half of the year that are de fined as having high earnings management is 48.07%,com5Due to space limitations,we do not report this result.-pared with 50.92%for firms listed in the second half of the year,although the difference is not significant. Thus,we document the in fluence of the lock-up period on earnings management.

We further compare the earnings management of VC-backed and non-VC-backed firms.We find that, similar to the results for the full sample,both discretionary accruals estimated by the cross-sectional modified Jones model and performance-matched discretionary accruals for VC-backed firms and non-VC-backed firms tend to increase first and then decline,reaching their highest point in the IPO year.Speci fically,fordiscretionary accruals estimated by a cross-sectional modi fied Jones model,the earnings management of VC-backed firms is significantly positive in both the IPO year and the post-IPO year,and is higher in the post-IPO year(the year of the lock-up period)than in the pre-IPO year.Although the earnings management of non-VC-backed firms is significantly positive in all three consecutive years,it is lower in the post-IPO year than in the pre-IPO year.The earnings management pattern of VC-backed firms is also similar for performance-matched discretionary accruals.It is significantly positive in the IPO year,not significantly negative in the pre-IPO year and positive in post-IPO year.The pattern of earnings management of non-VC-backed firms is slightly different.It is significantly positive in the IPO year and not significantly negative in the pre-IPO or the post-IPO year.In summary,the results of the discretionary accruals estimated by a crosssectional modi fied Jones model and performance-matched discretionary accruals show that earningsmanagement is lower in VC-backed than non-VC-backed firms before the expiration of the lock-up period, but the earnings management of VC-backed firms reverses after the expiration of the lock-up period.The earnings management of VC-backed firms is higher than that of non-VC-backed firms in the year the lockup period expires,although not significantly.

Table 2Variable definitions.

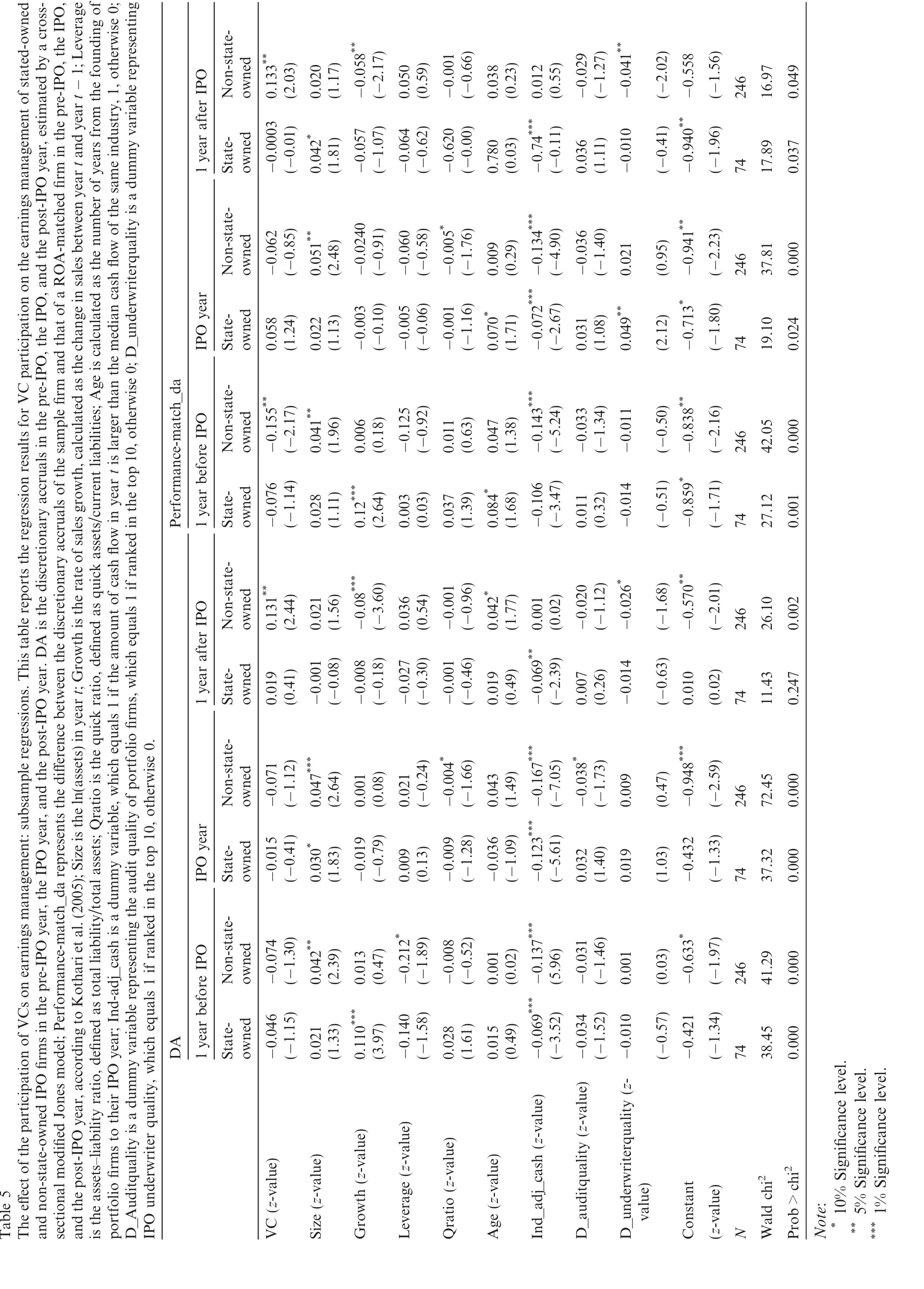

Table 3The effect of VCs on portfolio firms.This table presents the results for the effect of VC participation on portfolio firms.DA is the discretionary accruals in the pre-IPO year,the IPO year and the post-IPO year,estimated by a cross-sectional modified Jones model; performance-match_da represents the difference between the discretionary accruals of the sample firm and that of a ROA-matched firm in the pre-IPO year,the IPO year,and the post-IPO year,according to Kothari et al.(2005);Size is the ln(assets)in year t;Growth is the rate of sales growth,calculated as the change in sales between year t and t-1;Leverage is the assets-liability ratio,defined as total liability/ total assets;Qratio is the quick ratio,defined as quick assets/current liabilities;Age is calculated as the number of years from the founding of a portfolio firm to its IPO year;Ind-adj_cash is a dummy variable that equals 1 if the amount of cash flow in year t is larger than the median cash flow of the same industry,otherwise 0;D_Auditquality is a dummy variable representing the audit quality of portfolio firms; it equals 1 if ranked in the top 10,otherwise 0;D_underwriterquality is a dummy variable representing IPO underwriter quality;it equals 1 if ranked in the top 10,otherwise 0.

The size of VC-backed firms is smaller in all 3 years.The difference is significant at the 1%level in the pre-IPO year,but not significant in the other 2 years.The growth rate of VC-backed firms is higher in all 3 years, especially in the pre-IPO year,at the 5%significance level.Meanwhile,VC-backed firms are younger at the 5% significance level.This finding is in accordance with the Grandstanding hypothesis proposed by Gompers (1996),which suggests that to signal their IPO performance,younger VCs tend to take younger portfolio firms to IPO.VC-backed firms also have more reputable underwriters.The reputations of VC-backed firms are higher than those of non-backed firms at the 5%significance level,in accordance with the findings of Chemmanur and Loutskina(2007).This implies that VCs help portfolio firms with IPO marketing in China’s market.However,the reputations of their auditors are lower than those of non-VC-backed firms,because VCs tend to choose lower quality auditors for the convenience of earnings management.

Finally,due to the support of VCs,the IPO firms backed by VCs have higher financial flexibility,more short-term and long-term solvency,significantly lower financial leverage in the pre-IPO and the IPO year, and a higher quick ratio in all 3 years,significant at the 1%,1%and 5%levels respectively,and less adequate operational cash flow.

4.2.Regression results

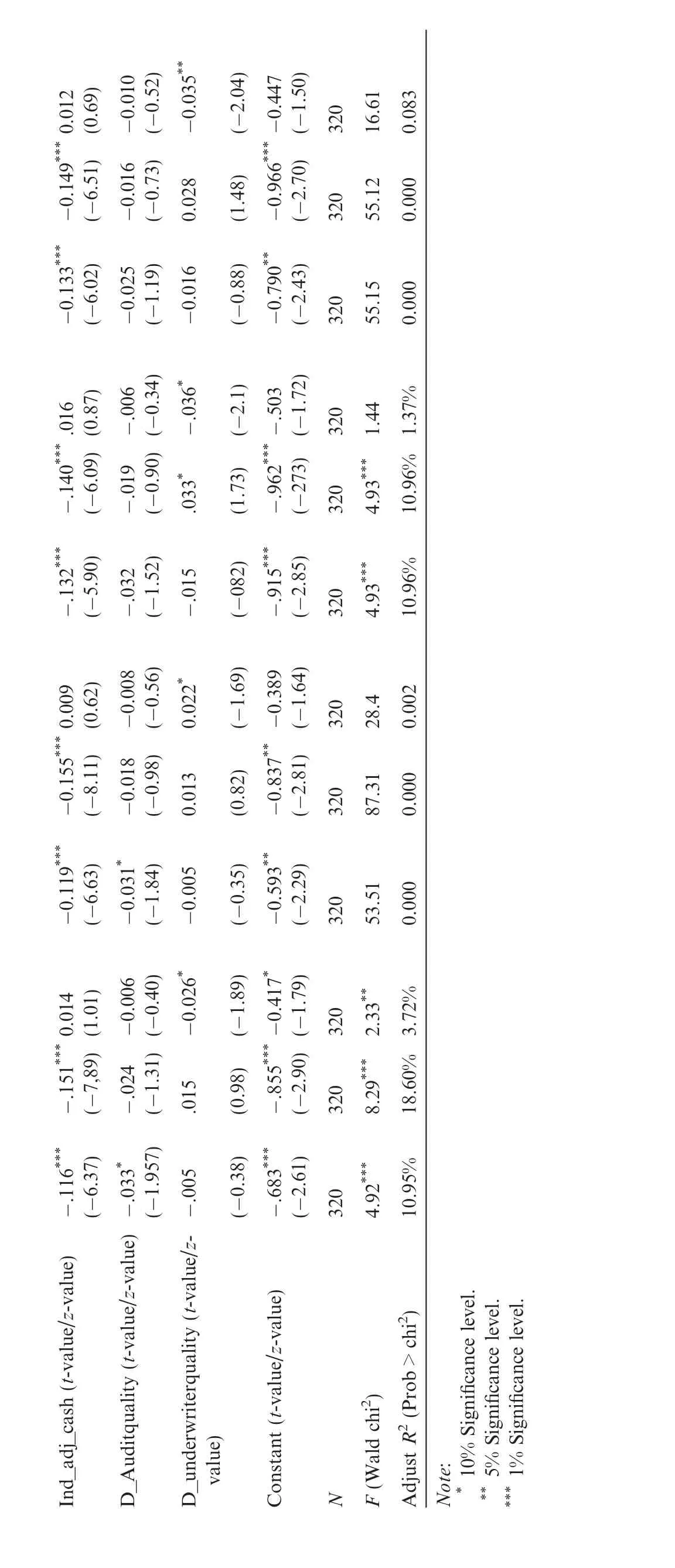

The regression results for Hypothesis 1,reported in Table 4,show that for all 3 years,VC has no significant effect on earnings management as measured by discretionary accruals(estimated by a cross-sectional modified Jones model)and performance-matched discretionary accruals,without controlling for the sample self-selection problem.The regression coefficients of discretionary accruals estimated by a cross-sectional modified Jones model(performance-matched discretionary accruals)on VC,a1,are-0.014(-0.009)and-0.014 (-0.007)in the pre-IPO and the IPO year,respectively,and 0.012(0.024)in the post-IPO year.All of these are non-significant,after controlling for sample firms’characteristics and underwriter and auditor reputation. However,if we consider the pattern over the 3 years,we can conjecture that VCs in China’s market tend to influence the management of portfolio firms by lowering earnings management before the expiration of the lock-up period.By reversing accounting earnings in the post-IPO year,they will realize higher investment returns when they cash in their equity at the end of the lock-up period.Thus,moral hazard plays a more important role than the certification/monitoring role.

The fifth to seventh and tenth to thirteenth column report the second-stage regression results of the treatment effect model,controlling for the sample self-selection problem.Due to space limitations,we do not report the first-stage probit regression results.In general,the overall LR chi2of the regressions are 49.8,50.33 and 49.56 for the 3 years,respectively.They are all significant below the 1%level and the Pseudo R2are 12.23%, 12.36%and 12.17%respectively.In all three probit regressions,the dummy variables-high-tech and geographical location-are significantly positive below the 5%level.

After controlling for the sample self-selection problem,the significance of the overall equation improves.In particular,in the regression for the post-IPO year,with performance-matched discretionary accruals as the dependent variable,the overall significance of the equation changes from insignificant to significant at the 10%level.The second-stage results show that VC participation affects the earnings management pattern before and after the expiration of the lock-up period.In the regression of discretionary accruals estimated using a cross-sectional modi fied Jones model,the regression coefficients a1remain insignificantly negative in the pre-IPO year and the IPO year,whereas the a1coefficient is 0.102 in the year the lock-up period expires and is significant at the 5%level.In the regression with performance-matched discretionary accruals as the dependent variable,the regression coefficient a1in the pre-IPO year is-0.136,significant at the 5%level. In the IPO year,the earnings management of VC-backed companies is still less than that of non-VC-backed firms.However,the difference is not significant,due to the increased earnings management by the firms listed in the first half of the year to boost accounting earnings after the expiration of the lock-up period.In the year the lock-up period expires,the participation of VCs has a significant effect on the earnings management ofportfolio firms,with the earnings management of VC-backed firms higher than that of non-VC-backed firms at the 10%significance level.

?

?

In addition,unreported results show that the ROA(industry-median-adjusted ROA)of VC-backed firms in the pre-IPO year is 14.2%(11.2%),which is significantly higher than that of non-VC-backed firms-11.9% (9%)-at the 1%(1%)level.In Table 3,we find that the growth rate of VC-backed firms in the pre-IPO year is 37%,compared with 29.2%for non-VC-backed firms.Therefore,reducing earnings management in the pre-IPO year will not have a significant effect on IPO pricing.If we consider the earnings management from the pre-IPO year to the post-IPO year together,we can infer that the participation of VCs reduces earnings management before the expiration of the lock-up period to reverse accounting earnings in the year the lock-up period expires.For this reason,under our current background,the imperfect market system means that VCs participating in IPOs have no incentive to monitor portfolio firms,their participation is more for speculative purposes.They collude with the management of portfolio firms or put pressure on the management to lower discretionary accruals before the expiration of the lock-up period in return for the reverse in accounting earnings once the lock-up period expires,which ultimately has a negative effect on the market.Thus,our empirical results support the moral hazard hypothesis.

The regression results also show that the earnings management of non-state-owned enterprises is higher than that of state-owned enterprises during the three consecutive years.In particular,in the regression model with discretionary accruals estimated by the cross-sectional modified Jones model as the dependent variable, the coefficients for VC in the IPO year and the post-IPO year are 0.045 and 0.037 respectively,both significant at the 5%level.This implies that the governance of state-owned enterprises is better than that of non-stateowned enterprises,in accordance with Gao and Cai(2011).In addition,larger firms have more resources to manage earnings,so they tend to have higher earnings management.The regression coefficients for discretionary accruals estimated by the cross-sectional modified Jones model(performance-matched discretionary accruals)on firm size in the pre-IPO and the IPO year are 0.036(0.035)and 0.042(0.052),significant at the 1%(5%)and 1%(1%)levels.Firms with lower growth rates have more incentive to increase growth by means of earnings management,which is more obvious in the year the lock-up period expires.The regression coefficients for discretionary accruals estimated by the cross-sectional modified Jones model(performancematched discretionary accruals)on growth are-0.071(-0.061)respectively,significant at the 1%(5%)level. Furthermore,older firms of lower quality(Xue,2002)tend to have higher earnings management.The regression coefficient for performance-matched discretionary accruals on age is 0.057,significant at the 10%level in the pre-IPO year.Meanwhile,firms with lower financial leverage receive less monitoring from debtors,which leads to higher earnings management.The regression coefficient for discretionary accruals estimated by the cross-sectional modified Jones model on financial leverage is-0.174,significant at the 5%level in the pre-IPO year.As predicted,firms with worse operational cash flow tend to have higher earnings management. Finally,auditors and underwriters do not inhibit earnings management.

Because VCs increase earnings in the year the lock-up period expires to obtain higher equity selling prices, high earnings management inevitably leads to more frequent equity selling.To test this direct result of earnings management,we analyze equity selling by VCs in the post-IPO year.The results show that 54 firms incur equity selling by VCs in the post-IPO year,accounting for 62.92%of the sample firms with lock-up periods of 1 year.Among them,18 firms(22.32%)incur equity selling on the day of the expiration of the lock-up period. Thus,the moral hazard hypothesis is further supported.

To investigate whether there is a different effect of VC participation on earnings management for firms with different ownership,we divide the total sample into state-owned and non-state-owned subsamples.The results before controlling for sample se6Because of space limitations,we do not report this result.lf-selection show that in general,the participation of VCs has no significant effect on earnings management.Speci fically,when the dependent variable is discretionary accruals estimated by the cross-sectional modi fied Jones model,the regression results for both state-owned and non-state-owned firms tend to be similar.In the pre-IPO and the IPO year,the participation of VCs has a negative relationship with earnings management,but the relationship turns positive in the post-IPO year,although not significantly. However,in the performance-matched discretionary accruals regression,the participation of VCs has apositive influence on the earnings management of state-owned enterprises in the three consecutive years.For non-state-owned enterprises,VC participation has a negative effect on earnings management in the pre-IPO year,but a positive influence in the other 2 years.

?

Table 5 shows the second-stage regression results after controlling for sample self-selection.Due to space limitations,we do not report the first-stage probit regression results.The overall LR chi2of the three regressions on the state-owned sample are 26.81,29.45 and 26.32 respectively,all significant below the 1%level.The Pseudo R2are 30%,32.96%and 29.46%respectively.The dummy variables-high-tech and geographical location-are significantly positive below the 1%level in the regressions for each of the 3 years.For nonstate-owned enterprises,the overall LR chi2for the three regressions are 34.85,35.49 and 35.36 respectively, all below the 1%level.The Pseudo R2are 10.79%,10.99%and 10.94%respectively.The dummy variableshigh-tech and geographical location-are also significantly positive in the regressions for all 3 years and significant below the 1%,1%and 10%levels.

According to Table 5,in the state-owned sample,the participation of VCs has a weak effect on earnings management in all 3 years.None of the regression coefficients for earnings management on VC a1are significant.In the regression of discretionary accruals estimated by the cross-sectional modified Jones model,it seems that VC participation weakly reduces earnings management in the pre-IPO and the IPO year,with the gap between VC-backed and non-VC-backed firms narrowing.In the post-IPO year,the earnings management of VC-backed firms is higher than that of non-VC-backed firms.For the regression of performance-matched discretionary accruals,none of the regression coefficients for earnings management on VC a1are significant.VC participation weakly reduces earnings management in the pre-IPO and the post-IPO years,and increases it in the IPO year.

For non-state-owned enterprises,VC participation significantly influences earnings management in the post-IPO year.In the pre-IPO year,VC participation reduces performance-matched discretionary accruals at the 5%significance level and also reduces discretionary accruals estimated by the cross-sectional modified Jones model.Although insignificant,the regression coefficients for discretionary accruals estimated by the cross-sectional modified Jones model(performance-matched discretionary accruals)on VC a1are-0.155 (-0.074).In the IPO year,the reduction in earnings management as a result of VC participation is further weakened.The regression coefficients for discretionary accruals estimated by the cross-sectional modified Jones model(performance-matched discretionary accruals)on VC a1are-0.071(-0.062),both not signif icant.However,in the post-IPO year,the participation of VCs increases the earnings management of portfolio firms and the regression coefficients for discretionary accruals estimated by the cross-sectional modi fied Jones model(performance-matched discretionary accruals)on VC a1are 0.131(0.133),significant at the 5%(5%) level.Combined with the discussion on Hypothesis 1,we believe that the participation of VCs in non-stateowned enterprises,compared with state-owned enterprises,has more effect on earnings management before and after the expiration of the lock-up period.Therefore,Hypothesis 2 is also supported.

We also conduct the following robustness tests: first,we use the Jones model to estimate earnings management;second,we measure firm size by sales;and third,we use growth in net income as a proxy for the growth of IPO firms.The results are consistent with those reported.

5.Conclusions

We use a sample of IPO firms in the SME Board and GEM between 2005 and 2009,and establish a twostage treatment effect model to control for the sample self-selection problem.We investigate the participation of VCs in the earnings management of portfolio firms in the year before IPO,the IPO year and the year after IPO.We reach the following conclusions.

(1)To increase accounting earnings in the year in which the lock-up period expires,the participation of VCs lowers earnings management,especially in the pre-IPO year,and increases earnings management in the post-IPO year.

(2)Compared with state-owned IPO companies,the participation of VCs has more effect on earnings management before and after the expiration of the lock-up period in non-state-owned enterprises.In the subsample of state-owned enterprises,VC participation has no significant effect on earnings managementfrom the pre-IPO year to the post-IPO year.However,for non-state-owned enterprises,the participation of VCs significantly reduces earnings management in the pre-IPO year.This results in a significant reversal in discretionary accruals estimated by the cross-sectional modified Jones model and performancematched discretionary accruals in the year of the expiration of lock-up period.

Thus,we provide a comprehensive investigation of the effect of the participation of VCs on the accounting information quality of IPO firms before and after the expiration of the lock-up period.We reach the conclusion that under China’s current institutional background,the involvement of VCs in IPO firms reflects a moral hazard role rather than a certification/monitoring role.This conclusion is important for the decision making of investors and policymakers.First,due to self-interest,the participation of VCs is more for speculative purposes.They collude with the management of portfolio companies or put pressure on the portfolio firms’management using their own professional advantages and social networks,to reduce earnings management before the expiration of the lock-up period and to reverse accounting earnings after the expiration of the lock-up period.Investors,therefore,should not blindly follow the behavior of VCs.Second,to increase the incentive of VCs to positively monitor their portfolio firms,regulators should not only strengthen the supervision of VCs and establish appropriate punishment mechanisms to regulate their speculative behavior,but should also establish guidance and motivation systems to increase VCs’motivation to obtain investment returns by providing R&D support,help with sales and purchase channels,management improvements and other valueadded services.Finally,government should improve the financing environment of non-state-owned enterprises and establish appropriate mechanisms to solve the problem of financing bottlenecks in non-state-owned enterprises so that the negative effects of venture capitalists’involvement in non-state-owned enterprises can be reduced.

As this paper does not test the effect of reputation and other characteristics of VCs on the accounting information quality of IPO firms,this would be an interesting future research direction.

Acknowledgment

This study was supported by the project“The Role of Private Equity in the GEM IPO”(No.FRF-TP-12-122A)funded by the Fundamental Research Funds for the Central Universities.

Agrawal,A.,Cooper,T.,2009.Accounting Scandals in IPO Firms:Do Underwriters and VCs Help?Culverhouse College of Business, University of Alabama.Working Paper.

Baker,M.,Gompers,P.,2003.The determinants of board structure at the initial public offering.Journal of Law and Economics 46,569-598.

Ball,R.,Shivakumar,L.,2005.Earnings quality in UK private firms:comparative loss recognition timeliness.Journal of Accounting and Economics 39,83-128.

Ball,R.,Shivakumar,L.,2008.Earnings quality at initial public offerings.Journal of Accounting and Economics 45,324-349.

Barry,C.,Muscarella,C.,Peavy,J.,Vetsuypens,M.,1990.The role of venture capital in the creation of public companies:evidence from the going-public process.Journal of Financial Economics 27,447-472.

Brandt,L.,Li,H.B.,2003.Bank discrimination in transition economies:ideology,information or incentives?Journal of Comparative Economics 31,387-413.

Bruton,G.D.,Ahlstrom,D.,2003.An institutional view of china’s venture capital industry:explaining the difference between China and the West.Journal of Business Venturing 18,233-259.

Cao,J.X.,2009.Are Buyout Sponsors Market Timers in RLBO?Singapore Management University.Working Paper.

Cohen,D.A.,Langberg,N.,2006.Venture Capital Financing and the Informativeness of Earnings.SSRN Working Paper.

Chemmanur,T.J.,Loutskina,E.,2007.The Role of Venture Capital Backing in Initial Public Offerings:Certification.Screening or Market Power.SSRN Working paper.

Chou,D.,Gombola,M.,Liu,F.,2006.Earnings management and stock performance of reverse leveraged buyouts.Journal of Financial and Quantitative Analysis 41,407-438.

Darrough,M.,Rangan,S.P.,2005.Do insiders manipulate earnings when they sell their shares in an initial public offering?Journal of Accounting Research 43,1-33.

Hochberg,Y.V.,2003.Venture Capital and Corporate Governance in the Newly Public Firm.AFA 2004 San Diego Meetings.

Gioielli,S.O.,Carvalho,D.,Antonio,G.,2008.The Dynamics of Earnings Management in IPOs and the Role of Venture Capital. Fundacao Getulio Vargas School of Business.Working Paper.

Gompers,P.,1996.Grandstanding in the venture capital industry.Journal of Financial Economics 42,133-156.

Greene,W.H.,2003.Econometric Analysis.Prentice Hall Business Publishing,Upper Saddle River,NJ.

Kothari,S.P.,Leone,A.J.,Wasley,C.E.,2005.Performance matched discretionary accrual measures.Journal of Accounting and Economics 39,163-197.

Katz,S.P.,2009.Earnings quality and ownership structure:the role of private equity sponsors.Accounting Review 84,621-658.

Lee,P.M.,Wahal,S.,2004.Grandstanding,certification and the underpricing of venture capital backed IPOs.Journal of Financial Economics 73,375-407.

Lerner,J.,1995.Venture capitalists and the oversight of private firms.Journal of Finance 50,301-318.

Morsfield,S.G.,Tan,C.E.L.,2006.Do venture capitalists influence the decision to manage earnings in initial public offerings?Accounting Review 81,1119-1150.

Sahlman,W.A.,1990.The structure and governance of venture-capital organizations.Journal of Financial Economics 27,473-521.

Scott,W.R.,1987.The adolescence of institutional theory.Administrative Science Quarterly 32,493-511.

Scott,W.R.,1995.Institutions and Organizations.Sage Publications,Thousand Oaks,CA.

Teoh,S.H.,Welch,I.,Wong,T.J.,1998.Earnings management and the long-run performance of initial public offerings.Journal of Finance 53,1935-1974.

Wongsunwai,W.,2007.Does Venture Capitalist Quality Affect Corporate Governance?Stanford Graduate School of Business.Working Paper.

Chen,G.,Yu,X.,Kou,X.,2011.The participation of VCs on the IPO discount of enterprises in China:a comparison of different markets. Economic Research Journal 5,74-85.

Fang,J.,2010.Are non-state-owned listed company discriminated in bank loan?Management World 11,123-131.

Gao,M.,Cai,W.,2011.Report on the Financial Governance Index of Listed Companies in China.Economic Science Press,BJ.

Hao,S.,Tao,H.,Tian,J.,2011.A comparison study of the state-owned enterprises of different ownership structures:take Shandong province as example.China Industrial Economic Journal 9,130-139.

Hu,Z.,Bu,Y.,2012.The Effect of Political Connection of Venture Capital on the Possibility of Successful IPO.University of Science and Technology of Beijing.Working Paper.

Li,P.,Shen,Y.,2010.The governance effect of media:evidence from China.Economic Research Journal 4,14-27.

Xu,H.,Chen,C.,2009.Accounting earnings quality,IPO pricing and long-term performance:evidence from the IPO after IPO reform. Management World 8,25-38.

Xue,S.,2002.How are the stock prices of loss listed companies determined?China Accounting and Financial Research 4,100-115.

Yu,Z.,Tian,G.,Qi,B.,Zhang,H.,2010.The corporate governance mechanism of media focus based on the view of earnings management.Management World 9,127-140.

30 December 2011

*Corresponding author.

E-mail address:huzy@manage.ustb.edu.cn(Z.Hu).