Thoughts on the Implementation Path to a Carbon Peak and Carbon Neutrality in China’s Steel Industry

2021-04-22 11:34RuiyuYinZhengdongLiuFngqinShnggun

Engineering 2021年12期

Ruiyu Yin, Zhengdong Liu, Fngqin Shnggun

1. The CO2 emission status of the steel industry in China

As an important basic sector of the national economy, China’s steel industry is a major energy consumer and a major emitter of carbon dioxide(CO2).Based on previous studies[1–3],Fig.1 shows a preliminary estimation of the CO2emissions of the steel industry in China from 1991 to 2019.

From Fig. 1, it can be seen that:

(1) Due to the rapid growth in crude steel production,the total CO2emissions from the steel industry in China have increased from 278 million tonnes in 1991 to 1.625 billion tonnes in 2019. However, this increase in total CO2emissions (4.85 times) is much lower than the increase in steel production(13.02 times).Furthermore, the proportion of emissions from the steel industry is 15%–17% of China’s total CO2emissions.

(2) From 1991 to 2019, the specific CO2emissions per tonne of steel in the steel industry in China decreased from 3.91 tonnes in 1991 to 1.63 tonnes in 2019, for an overall decrease of 58%.

(3) The total CO2emissions from the steel industry in China reached an inflection point in 2014, at a peak of 1.731 billion tonnes, and then began to exhibit a downward trend. However,comparing with 2014, the output of crude steel reached 1.065 billion tonnes in 2020, and, as a result, the total CO2emissions from the steel industry are predicted to reach a similar peak of 1.738 billion tonnes.It can be seen that there is a strong correlation between the steel industry’s carbon peak and its crude steel output.

These three points demonstrate that the steel industry in China has made significant progress in energy saving and emission reduction in the past three decades.However,due to the relatively large output of crude steel in China, the steel industry’s share of CO2emissions out of the total national CO2emissions is still relatively high. In the future, in order to realize China’s carbon emission reduction commitments,the steel industry must take the path of decarbonization.

Fig. 1. Changes in crude steel output, total CO2 emissions, and specific CO2 emissions per tonne of steel in China’s steel industry from 1991 to 2019.

2.The understanding of‘‘carbon peak’’and‘‘carbon neutrality’’in the steel industry

The total CO2emissions from the steel industry depend on the specific CO2emissions per tonne of steel and the total crude steel output of the steel industry:

where Cemissionrepresents the total CO2emissions from the steel industry,I represents the specific CO2emissions per tonne of steel from the steel industry,and P represents the total crude steel output from the steel industry.

It can be seen from Fig.1 that it is relatively easy to achieve a carbon peak in the steel industry,and a peak may have been achieved in 2014.Of course,due to the rapid growth in crude steel output in recent years,there may be a new peak.It can be said that,although reaching a carbon peak is not difficult,realizing a decline in carbon emissions is not easy. This is because reaching a carbon peak and achieving a decline in carbon emissions do not entirely depend on the steel industry itself. The carbon peak of the steel industry depends not only on the specific CO2emissions per tonne of steel(including the ratio between the blast furnace–basic oxygen furnace(BF–BOF)process and the full-scrap electric arc furnace(EAF) process), but also on the total output of crude steel, and the latter depends on the development level of the national economy and on investment orientation.For this reason,it has been preliminarily judged that the carbon peak time node of the steel industry in China occurred in 2014, or the early period of the 14th Five-Year Plan(Fig.2).If the steel industry can prevent its carbon emissions from surpassing the 2014 peak and thereby set its carbon peak as having already occurred in 2014,it will be possible to achieve a decline in carbon emissions more rapidly and reach carbon neutrality sooner.

In terms of the absolute quantity of CO2emissions from the steel industry, it is extremely difficult for the steel industry to achieve carbon neutrality on its own.However,if the coordination of society as a whole is considered, including the adoption of carbon capture, utilization, and storage (CCUS) technology, the use of renewable energy, increasing carbon sinks, and launching inter-industry carbon-trading measures, it may be possible for the steel industry to achieve carbon neutrality in the future.

3. Ideas for achieving a carbon peak and carbon neutrality in China’s steel industry

To achieve a peak in carbon emissions and eventually reach carbon neutrality in the steel industry, we provide the following ideas:

(1) The steel industry in China must first adjust its industrial structure from a macroscopic perspective, reduce its total crude steel output,and eliminate backward technologies and equipment.It should not continue to increase the total crude steel output or export large quantities of low-value-added steel products. A high-quality but reduced-quantity development path should be taken.

(2)Steel plants should take a green development path of energy conservation,emission reduction,and decarbonization.At present,we must attach great importance to decarbonization, which includes the following aspects:

· Decarbonization of resources: use fewer resources, and promote the rational use of scrap in particular.

· Decarbonization of energy: use less or no fossil energy,switch to electricity,and make full use of power grid abandonment in particular.

· Decarbonization of the manufacturing process: start with the transformation of the production process for long products for construction, as these long products can mainly be produced by the full-scrap EAF process. In addition, city steel plants that use scrap collected from urban sources, as a form of so-called ‘‘urban mining,’’ should be rationally laid out.

· Decarbonization of the import and export trade: restrict the total export volume of high-carbon-load products such as coke, ferroalloys, and low-value-added steel products through taxation, quotas, and other measures.

· Decarbonization of policies and regulations: implement carbon trading by industry; levy carbon taxes by phases,by products, and by manufacturing processes; and establish decarbonization legislation. It can be seen from the successful experience of achieving ultra-low emissions in the steel industry that a series of supporting policies are a powerful lever to achieve goals. It seems that close attention must be paid to carbon allowances, carbon trading,carbon taxes, carbon negative lists, carbon planning, and decarbonization legislation.

Through supply-side structural reforms,the optimization of the industrial structure of the national economy can be promoted and carbon emissions from high-energy-consuming manufacturing,energy, and transportation industries can be reduced. At the same time, carbon sink capabilities should be strengthened and improved.

(3) The production manufacturing process structure of the steel industry in China should be adjusted in regard to the development process of reduction. The full-scrap EAF process should be used to produce long products for construction, instead of using medium and small BF-BOF to produce bulk products such as rebars and wire rods. Then, so-called ‘‘urban mines’’ can be utilized and city steel plants can be developed with an appropriate layout. This measure has great potential for decarbonizing the steel industry.

Fig. 2. Judgment of key time nodes for achieving a carbon peak (or peaks) and carbon neutrality in the steel industry in China.

(4)For some large integrated steel plants that produce flat steel,it is necessary to further develop energy-saving and decarbonization technologies to reduce total CO2emissions.

4. Technology roadmap for China’s steel industry to achieve carbon neutrality

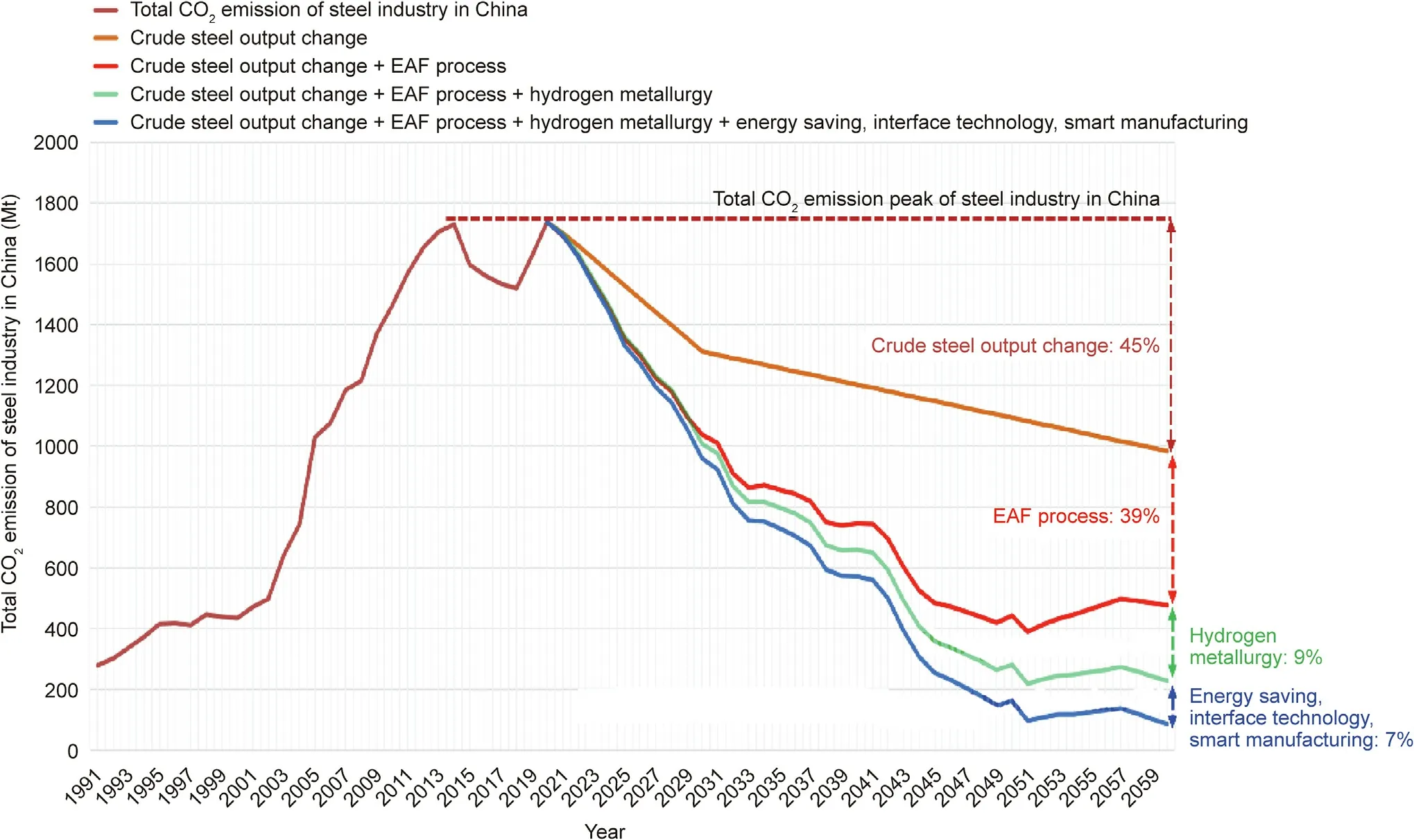

Assuming that the output of crude steel from 2021 to 2060 will decrease in equal steps, the output will be 800 million tonnes in 2030 and will then further decrease to 600 million tonnes in 2060. All scrap [4–6] can be concentrated in production based on the EAF process, while considering the impact of the adjustment of the electric energy structure on the level of CO2emissions from the EAF process. The production process share of hydrogen metallurgy (hydrogen reduction plus the EAF process) is 3% in 2030, 8%in 2040, 15% in 2050, and 25% in 2060. Furthermore,the potential for energy saving in the future is 10% [7,8], the potential for interface technology optimization is about 35 kilograms of coal equivalent (kgCE) per tonne of steel, and the potential for smart improvement is 12%. To avoid double counting with the building materials industry, the comprehensive utilization of metallurgical slag resources is not considered at present. Based on these assumptions, a technical roadmap to achieve carbon neutrality for the steel industry in China is provided (Fig. 3).

As shown in Fig. 3:

(1)Carbon emissions from China’s steel industry have entered a peak platform period. It is possible for the carbon peak of the steel industry in China to have been achieved in 2014,or the early period of the 14th Five-Year Plan,with a peak value of 1.7 billion–1.8 billion tonnes.

(2)If all of the suggested measures are adopted,the steel industry in China will emit about 100 million tonnes of CO2by 2060.However, if carbon capture, utilization, or storage (CCUS), carbon sinks,or carbon-trading measures were adopted,carbon neutrality in the steel industry will be expected to be achieved.

(3)Of the cumulative reduction in CO2emissions from the steel industry from 2021 to 2060,crude steel production factors account for about 45%,full-scrap EAF process factors account for about 39%,hydrogen metallurgy factors account for about 9%,and energy saving, interface technology, smart improvement, and other factors account for about 7%.

5. Conclusions

Our thoughts on the implementation of a carbon peak and carbon neutrality in China’s steel industry can be summarized in four main points:

(1) In general, the main measures needed in order for the steel industry to reach a carbon peak are to reduce the crude steel output and to reduce CO2emissions. Here, it should be emphasized that increasing the crude steel output will run counter to efforts to achieve a peak in carbon emissions. Reducing CO2emissions and reducing the crude steel output are also the main measures to achieve carbon neutrality, while increasing the carbon sink is a necessary supplement.

(2) The carbon peak time point of the steel industry is mainly determined by the peak value of the crude steel output.According to preliminary judgment, the carbon emissions from China’s steel industry have entered a peak platform period. The carbon peak time node of the steel industry in China occurred in 2014, or the early period of the 14th Five-Year Plan, with peak CO2emissions of 1.7 billion–1.8 billion tonnes. If the steel industry can prevent its carbon emissions from surpassing the 2014 peak and thereby set its carbon peak as having already occurred in 2014, it will be possible to achieve a decline in carbon emissions more rapidly and reach carbon neutrality sooner.

(3)It is extremely difficult for the steel industry to achieve carbon neutrality on its own; however, if the coordination of society as a whole is considered,it may be possible to achieve carbon neutrality in the steel industry.

Fig. 3. Technology roadmap for China’s steel industry to realize carbon neutrality.

(4) Reducing the total output of crude steel and adjusting the process structure and development of full-scrap EAF process steel plants are the two major measures that can enable the steel industry in China to achieve carbon neutrality. Other technologies can make limited contributions to reduce carbon emissions.

- Engineering的其它文章

- The Intelligent Beijing–Zhangjiakou High-Speed Railway

- Mechanisms of Steatosis-Derived Hepatocarcinogenesis: Lessons from HCV Core Gene Transgenic Mice

- Microneedle Makers Seek to Engineer a Better Shot

- Battery Recycling Challenge Looms as Electric Vehicle Business Booms

- Global Top Ten Engineering Achievements 2021

- Biomedical Engineering: Materials, Devices, and Technological Innovation Continue to Build a Better Future for Humankind